IMPORTANT UPDATES

OVERVIEW

School districts throughout the nation have experienced a decline in student enrollment since the COVID-19 pandemic of 2020. According to the Indiana Business Research Center, approximately 82% of Indiana counties have experienced decreases in their school-age populations. The reasons cited for declining enrollment across the state include shifting economic conditions, declining birth rates, increased enrollment in charter schools, and expanded access to school choice vouchers for non-public (private) schools.

Fayette County School Corporation has not been immune to these statewide and national trends. Over the past decade, our community has experienced a decline in student enrollment consistent with broader demographic patterns in Indiana. Contributing factors include lower birth rates over the past two decades, an aging population, and increased educational choice options available to families.

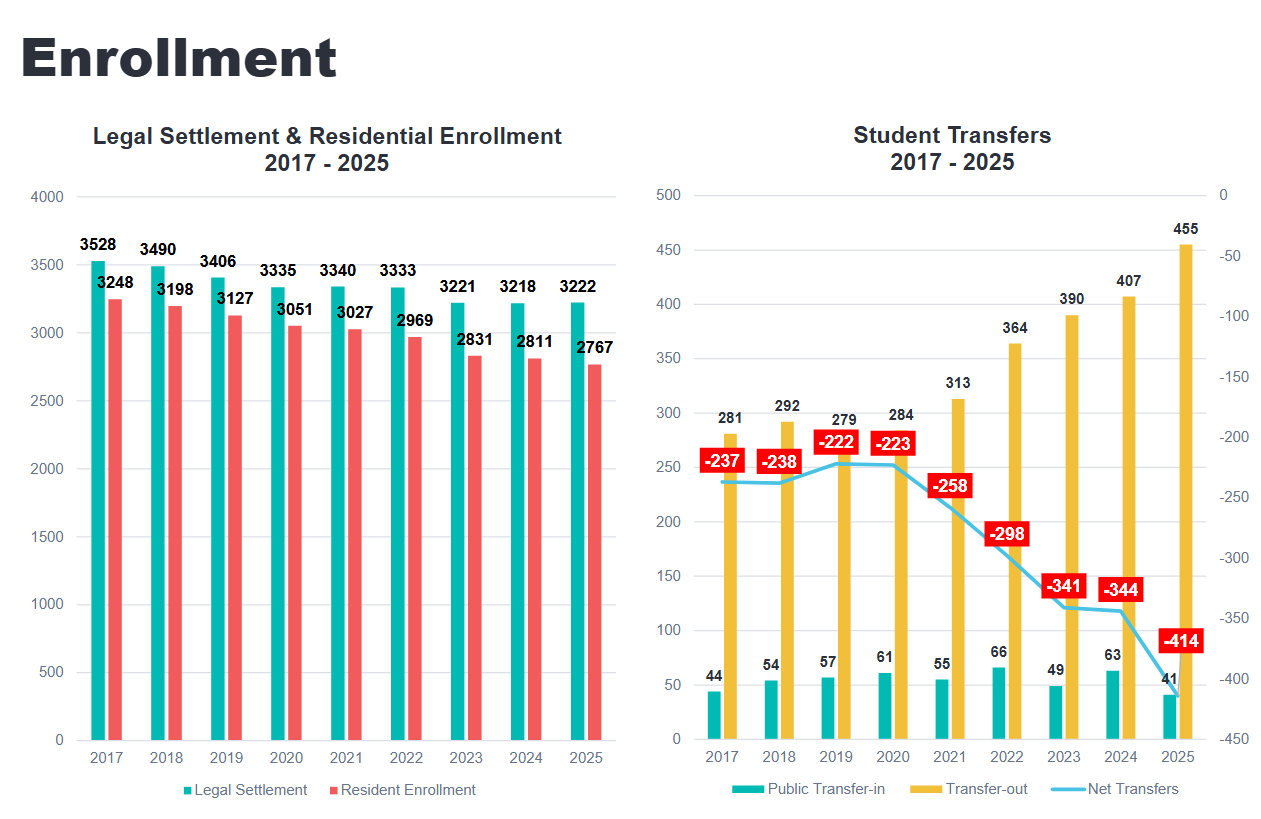

For the past decade, the Fayette County School Corporation has seen a reduction of close to 58 students per year. The total loss over the last 11 years has been 626 students. This has resulted in a loss of more than $5 million in funding annually in tuition support dollars.

GROWING COSTS & SHRINKING STUDENT POPULATION

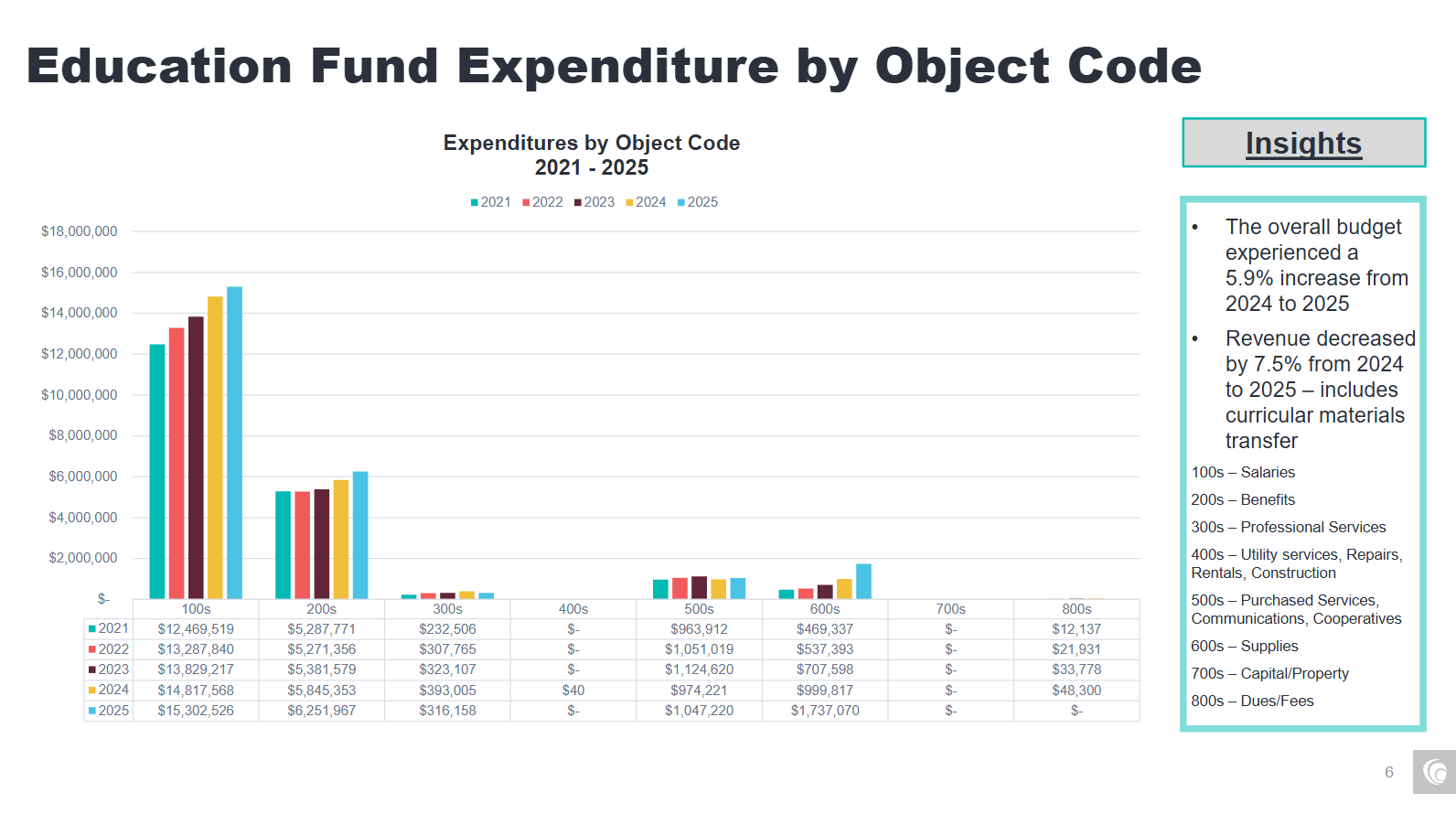

Over the past 11 years, multiple factors have caused FCSC’s enrollment to decline by approximately 19% (626 students), resulting in a loss of around $5 million of revenue in the Education Fund, which is what pays for teacher wages and benefits. Meanwhile, total payroll expenses for all employees have increased substantially during the same time period.

PROPERTY TAX REFORM AND ITS IMPACT

The Indiana General Assembly in 2025 enacted several significant changes to the way schools are funded, namely through SEA 1. This is not unique to the Fayette County School Corporation and every school corporation across the state will feel this impact. Over the past several months, we have been carefully studying the new legislation and its impact on our schools.

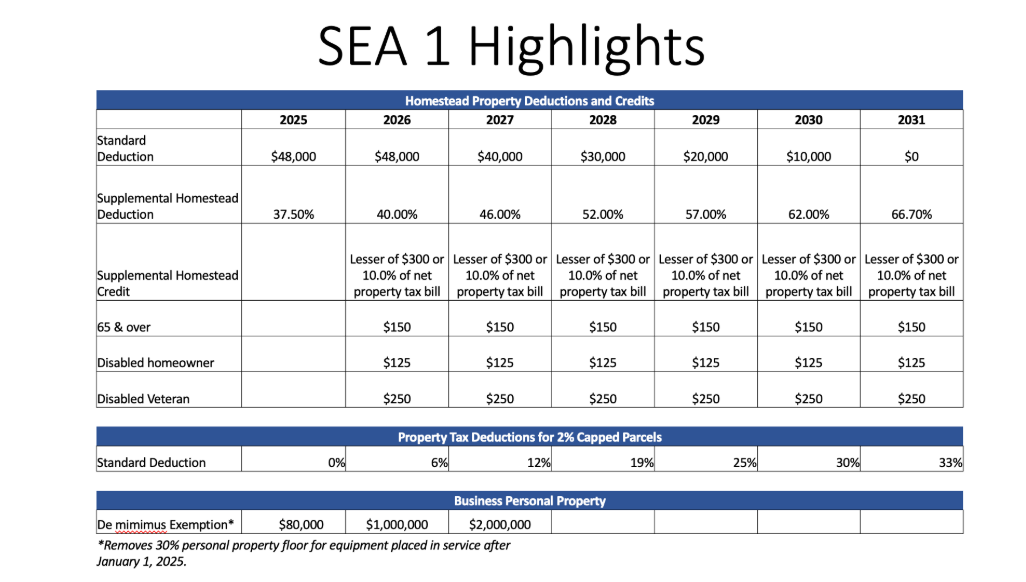

Key Property Tax Changes Under SEA 1

1. Standard Homestead Deduction Changes

The current flat dollar homestead deduction (such as $48,000) will be gradually reduced and eventually eliminated.

2026: $40,000

2027: $30,000

2028: $20,000

2029: $10,000

2030: $0

Over time, less of a home’s value will be automatically deducted before taxes are calculated.

2. Supplemental Homestead Deduction Changes

The supplemental deduction becomes a percentage of assessed value instead of a flat structure.

The percentage increases gradually:

2026: about 43%

2027: about 48%

2028: about 53%

2029: about 58%

2030: about 62%

2031 and after: about 66.7%

A larger percentage of a home’s assessed value will be shielded from taxes over time.

3. Supplemental Homestead Credit (New Credit)

Homeowners receive a credit equal to 10% of their homestead property tax bill.

The credit is capped at $300.

This reduces the final tax bill directly (not just the assessed value).

4. Credits for Those 65 and Over and Disabled

Existing deductions for seniors and disabled homeowners are converted into credits.

Over-65 credit: up to $150 (income limits apply).

Blind/disabled credit: up to $125.

These credits directly lower the amount owed.

5. Changes to 2% Capped Parcels

A new deduction applies to properties subject to the 2% property tax cap (such as rentals and farmland).

The deduction phases in over time and reduces taxable assessed value.

This lowers the overall tax base for those properties.

6. Business Personal Property Floor Changes

The exemption threshold for business personal property increases to $2 million.

Many small businesses will no longer pay this tax.

The 30% depreciation floor for new equipment is eliminated.

New business equipment can depreciate below 30% of original cost.

This reduces taxable business property value.

What This Means for FCSC

Schools rely on property taxes for debt service, operations, transportation, and referenda funds.

As deductions and credits increase, taxable assessed value decreases.

Lower taxable value generally means less local property tax revenue.

Schools may face tighter budgets or need to adjust long-term financial planning.

Referendum timing and rules are also more limited under SEA 1.

FEBRUARY 24th, 2026 BOARD OF SCHOOL TRUSTEES MEETING

FINANCE AND FACILITY PLANNING OVERVIEW

FREQUENTLY ASKED QUESTIONS